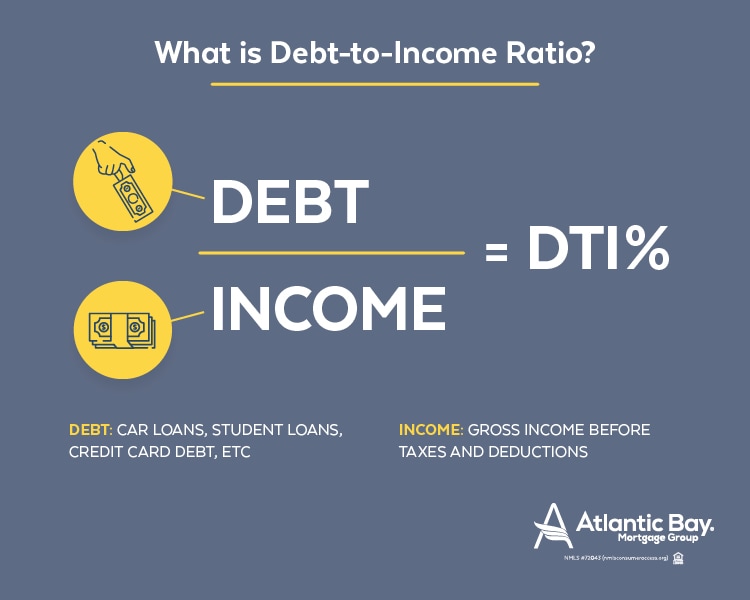

If you find it's too difficult, you'll know you require to change your expectations downward. Home mortgage loan providers consider not simply your credit however also your debt-to-income ratio when you obtain a loan. This ratio compares overall debt payments to your gross regular monthly earnings. For instance, if your gross monthly earnings is $4,000, your mortgage will cost $1,000 regular monthly and all other financial obligations add up to $500, your debt-to-income ratio is $1,500/$ 4,000 or 37.

Generally, your debt-to-income ratio can't exceed 43% to get approved for a home loan, although numerous lenders prefer a lower ratio. If you owe a great deal of cash, you're going to need to pay for some of it to get approved for a loan to purchase a house. Paying down financial obligation likewise assists enhance your credit, which allows you to receive a better home loan rate and lower monthly payments and interest.

Typically, you'll require: Proof of earnings: This can consist of tax returns, pay stubs, W2s from companies, and 1099s if you're an independent professional. You'll require to show you have actually had stable income for two years. If your earnings was $50,000 each year up until just recently and simply went up to $100,000, your loan provider might only "count" $50,000 in identifying what you can obtain.

Bank and brokerage declarations offer evidence of assets. You'll require numerous other documents after you actually find a home, including an appraisal, a study, proof of insurance coverage, and more. But offering standard monetary documents early is essential so you can be pre-approved for a loan. Pre-approval makes you a more competitive house buyer given that sellers know you can really get approved for funding.

If you get your monetary life in order initially, purchasing your home should be a good experience that assists enhance your net worth-- rather than a monetary mess that originates from getting stuck to an expensive loan that's hard to pay back.

Anxious about getting a mortgage? You're not alone. Consumer research studies have discovered that getting a very first home mortgage ranks quite high on the stress scale; it's right up there with going to the dentist or getting pulled over for driving too quick. Luckily, though, a little mortgage understanding can go a long way towards minimizing your anxiety and helping you to get a better mortgage.

Home mortgage down payment minimum variety from 0% (for VA home loans and Rural Housing home loans) to 20 percent (for non-government loans with no home loan insurance), with plenty of options in between. There are 97% home loans for debtors with above-average credit rating (the Conventional 97) and there are loans requiring simply 3.

Not known Details About What Are Interest Rates For Mortgages

Furthermore, there is the piggyback home loan for purchasers with 10 percent to put down, plus a host of other alternatives including three percent down programs from Fannie Mae and Freddie Mac, and programs such as HomeReady. You do not require to make a downpayment of 20% to acquire a house. Yes, to qualify for the majority of lenders' advertised rates, you need a large down payment and excellent credit rating.

For instance, the Federal Housing Administration (FHA) insures home mortgages for borrowers whose credit history vary as low as 500. And, sometimes, the FHA will insure loans for debtors without any credit rating whatsoever. In addition, Fannie Mae and Freddie Mac, which buy and sell most of house loans in the U.S., allow FICO scores to 620, as does the Department of Veterans Affairs with its VA loans; and the U.S.

Some home loan lenders authorize loans with scores under 600. When you purchase property, there are costs which are a part of the transaction. There are escrow charges, title insurance charges, lender costs, house appraisal services, home inspections, and more. Overall, closing costs are lower than what they used to be, but costs can still build up.

Ask the seller to pay your costs. It should not matter whether you how much are timeshares pay $295,000 for a house and pay your own expenses, or use $300,000 and ask the seller to pay $5,000 of your expenses. Or, ask the lender to pay your expenses. A lot of lending institutions will consent to this, however you'll be asked to pay a greater home loan rates of interest.

25%) increase in your rate will cover your expenses completely. This is called a zero-closing cost home mortgage loan. Last but not least, you can ask the government to pay your costs. Many novice buyer programs consist of assist with closing expenses. Some even use deposit help Look at this website as well. Ask a home mortgage loan officer what type of work history is needed to get authorized for a home mortgage, and the automatic response will be "two years." That's kinda sorta true, however not completely.

Someone who worked as an unsettled engineering intern, and was later on provided a full-time, employed position is more likely to get authorized than a candidate whose work history includes full-time bartending, followed by a stint at a day care facility, then by part-time barista work and multi-level marketing. This does not mean that both borrower types won't be authorized, it simply suggests that you never understand up until you ask.

Call a lending institution and ask to be pre-approved for a home loan. You'll discover just how much you certify to obtain, what it will cost, and if there is anything you can do to borrow more, or to pay less. Pre-approvals can be finished in a couple of minutes. Almost all U.S.

The Ultimate Guide To How To Qualify For Two Mortgages

The procedure doesn't need to make you nervous, though the more you understand, the much better off you'll be. Get today's live home loan rates now. Your social security number is not required to begin, and all quotes include access to your live home loan credit scores.

Deciding to become a homeowner can be demanding for numerous novice homebuyers. The looming questions of michael yaros price, where to acquire, and task security are all genuine concerns that warrant severe consideration. The reality is that there's never a correct time or the ideal scenarios to begin this journey, however ultimately, you wish to deal with house-hunting and the home loan procedure as you would other major life occasions.

Here are 5 crucial aspects every novice homebuyer must think about when getting a home mortgage. In a current S&P/ Case-Shiller report, house rates increased 5. 2 percent. Even with a steady labor market that supports the rate increase, house costs continue to climb faster than inflation firing up competition for fewer available houses (how do mortgages work in monopoly).

Given, when stock is low, it does end up being a sellers' market making it harder for purchasers to complete, however dealing with a skilled-lender who can assist facilitate the debtor through the procedure is vital to getting approval. When purchasing a home, employing a team of experts is a significant component that could identify the success or death of your mortgage experience.

Bond encourages that when looking for a home loan, make sure that your taxes are filed and arranged. Gather your last month of paystubs and make certain you can easily access the last two months of your bank accounts. You ought to likewise acquire a letter of work from human resources, and check your credit report to figure out if there are any discrepancies.